Want to be in the loop?

subscribe to

our notification

Business News

EMERGING TRENDS IN VIETNAM’S REAL ESTATE MARKET 2025

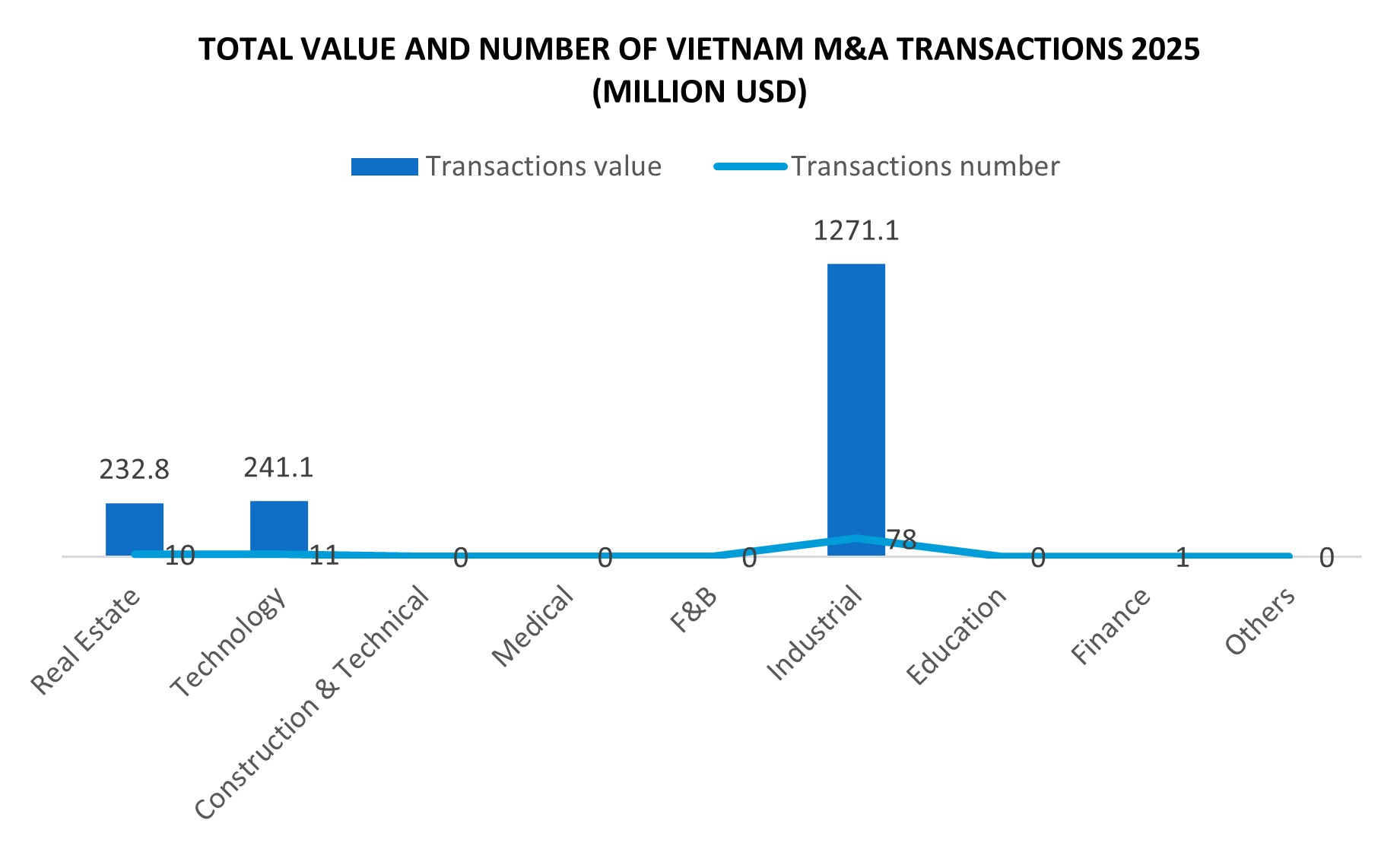

Source: Capital IQ, Grant Thornton.

Vietnam has set an ambitious GDP growth target of 8.3–8.5% for 2025, expected to drive strong momentum across the green economy, digital economy, and digital transformation, particularly in mergers and acquisitions (M&A).

The “Emerging Real Estate Trends in Vietnam 2025” report, recently released by Indochina Strategic—the real estate advisory arm of Indochina Capital (ICC)—highlights 10 emerging trends shaping Vietnam’s real estate M&A market.

Rapid expansion accelerates corporate investment, diversification, and market consolidation. Domestic firms look to scale operations while foreign investors seek faster entry, making M&A a natural growth channel. In the first eight months of 2025, total registered FDI reached US$26.14 billion, up 27.3% year-on-year, with manufacturing accounting for 37% of capital contributions and share purchases, at nearly US$1.7 billion.

High growth projections suggest improving consumer demand, rising capital inflows, and stronger investor confidence. This encourages M&A as companies seek modern technologies, entry into high-potential sectors, and supply chain resilience. Key drivers include favorable macroeconomic conditions and the new Land Law, effective from August 2024, which enhanced transparency and created growth momentum. In August alone, 18 transactions were recorded with a value of US$2.23 billion, mainly in industrial, technology, real estate, and financial services. Domestic investors dominated in deal count, while international investors led large-scale transactions.

Ten trends shaping Vietnam’s real estate market in 2025

Trend #1: Lower Rates, Higher Dealflow

By August 2025, real estate credit showed recovery, supported by improved market conditions and government measures, though challenges remained with large bond maturities and high developer costs. The State Bank of Vietnam raised its credit growth target to stimulate the economy, focusing lending on priority sectors such as affordable housing. Banks lowered lending rates to 7–9%, improving access for both borrowers and investors. Over the past two years, new credit has mainly flowed to developers, funding acquisitions, restructuring, and rollouts after M&A. For buyers, stronger access to credit enables them to target land banks with clear legal status but limited capital or to acquire equity stakes in existing projects, while developers unable to secure financing turned to M&A as an indirect capital-raising tool.

Robust credit growth is a catalyst for restructuring, empowering strong developers to consolidate the market. Foreign investment has also rebounded strongly in H1 2025, further reinforcing confidence in Vietnam’s real estate market. Regionally, global financing remains pressured by high U.S. rates, but Vietnam’s macro stability and improving credit access support renewed M&A activity.

Trend #2: Banks Driving Asset Repricing

Across Asia-Pacific, lenders are pressing asset owners to reprice, reduce leverage, and inject equity, forcing many to lower asking prices. Vietnam contrasts with accommodative policies since 2023, stabilizing deposit rates and reducing lending costs. By August 2025, credit expanded by 9.9% year-on-year, with a 16% annual target. Average lending rates remain favorable at 7–9%, supporting acquisitions and project execution. However, this supportive environment is challenged by inflation (around 3–3.3%) and exchange rate volatility caused by gold price surge and the appreciation of the U.S. dollar, narrowing space for further easing. Overall, credit policies create pressure and opportunity for repricing and consolidation.

Trend #3: Industry Leads, Real Estate and Tech Remain Strong

Legal reforms and supportive policies, including the new Land Law, have stabilized credit conditions, improved transparency, and supported growth. In August, 18 deals valued at US$2.23 billion far exceeded July’s US$786 million, despite fewer transactions. Industrial real estate leads M&A, supported by an 8.9% rise in the industrial production index. Vietnam’s strategic location and China+1 strategy attract global manufacturers and logistics players. Major infrastructure projects—bridges, airports, and high-speed rail—strengthen connectivity, while reforms shorten project timelines. Industrial real estate continues to attract FDI, driving rental growth and M&A.

Trend #4: Resilience of Hospitality Market

Vietnam welcomed 12.2 million international visitors in the first eight months of 2025, up 22.5% year-on-year, with tourism projected to reach US$31.84 billion by 2030. Visa reforms extended stays to 45 days and introduced a 10-year Golden Visa. National celebrations, such as the 50th anniversary of Unification Day and the 80th anniversary of the August Revolution and National Day, boosted tourism. Hanoi alone generated US$85.8 trillion in tourism revenue. Nationwide hotel occupancy averaged 59%, indicating that Vietnam’s hospitality market is steadily “heating up”.

Examples like Indochina Capital’s Wink Hotel chain highlight growth potential. In just six years, its portfolio has expanded to six operating hotels across Vietnam. Reforms, including the 2024 Land Law and Resolution 68/NQ-CP, provided legal frameworks for condotels and resort villas, removing bottlenecks and restoring confidence. Former provinces like Phu Yen, Binh Dinh, and Quang Nam–Danang City are emerging hubs for resorts, while Hanoi and HCMC lead in urban hotels.

Trend #5: Social Housing and Residential

By mid-2025, 692 social housing projects were underway, totaling 633,559 units. Of these, 146 were completed, 124 under construction, and 422 approved, according to the Ministry of Construction. This progress reached nearly 60% of the 2021–2030 target of one million units. Social housing increases supply, reduces price pressure, stabilizes the market, and supports productivity and investment attraction.

Trend #6: High Return Expectations Across Investor Groups

Return expectations vary by investor type. Global funds show the highest appetite, with 20% targeting elevated returns. Regional funds and developers are more moderate at around 15%, balancing yields with stability. Japanese institutional investors are most conservative, with only 10% seeking high returns, reflecting their preference for low-risk, stable income assets.

Trend #7: New Economy Assets in Favour

Alternative assets continue attracting capital, with data centers among the most active segments. Rising digitalization and demand for cloud services fuel growth. Vietnam is increasingly competitive due to its young population, FDI in technology, and renewable energy capacity. Though nascent compared to peers, Vietnam’s data center sector has significant growth potential. Rental real estate has also grown steadily since 2017 and will likely continue through 2029, driven by urbanization and foreign professionals. Together, digital infrastructure and rental housing reflect dual growth drivers: urban development and digital transformation.

Trend #8: Rising construction costs

Across Asia-Pacific, construction and labor costs are rising sharply, delaying projects. Vietnam, however, has maintained relatively stable costs, with limited growth in labor and materials. Developers benefit from competitive tendering, giving Vietnam an edge for foreign investors in a region constrained by high development costs.

Trend #9: AI – Digital Real Estate Revolution

Artificial Intelligence (AI) is transforming project development and management, enabling tailored projects and enhancing smart city operations. In Vietnam, pilot programs include AI for project management, smart building automation, VR customer experiences, and brokerage support. In industrial real estate, AI helps with energy management, security, and cost savings. AI also shortens M&A deal timelines, opening potential for faster transactions. To maximize AI benefits, Vietnam needs a clear legal framework on data privacy and protection. At the same time, the technological shift poses challenges for the real estate workforce, requiring continuous upskilling to adapt to an increasingly digitalized environment.

Trend #10: Sustainability as a top priority

Sustainability is now central to investment decisions. ESG-driven capital is flowing into green projects, industrial parks, and housing. Vietnam targets net-zero emissions by 2050, and over 85% of the country’s fastest-growing firms have ESG commitments. Decree 80/2024/ND-CP on Direct Power Purchase Agreements supports renewable energy. Administrative mergers and infrastructure upgrades unlock new development opportunities in areas like Haiphong and peri-urban Hanoi and HCMC.

Challenges include valuation gaps, regulatory complexity, and integration risks, but fundamentals—urbanization, young demographics, housing demand, and resilient FDI—position Vietnam as one of Asia’s most attractive real estate M&A markets, where sustainability is a necessity.

Source: The Saigon Times

Related News

MEMBER CORNER / PROMOTIONS

VIETNAM'S MANUFACTURING STORY HAS CHANGED IN 2026

Vietnam is no longer attracting investment solely because of its competitive costs. Today, global manufacturers are increasingly choosing Vietnam for its expanding industrial ecosystem, resilient supply chains and growing role in high-value sectors such as semiconductors, electronics and advanced manufacturing.

BANKING / FINANCE / INSURANCE / TAX

VIETNAM NEEDS OVER $200BN FROM STOCK MARKET IN NEXT 5 YEARS

Speaking at the event, Bui Hoang Hai, vice-chairman of the State Securities Commission of Vietnam, said total investment demand in the 2026-30 period is estimated at VND38,000 trillion ($1.4 trillion). The state budget can only provide approximately VND8,500 trillion ($323 billion), or 20 percent, leaving the remaining 80 percent to be sourced from private and international capital.

VIETNAM ECONOMY INVESTMENT

HUNG YEN BUILDS DIGITAL FOUNDATIONS TO DRIVE LONG-TERM GROWTH

From strengthening data infrastructure to developing AI platforms, Hung Yen province is enhancing governance capacity while laying the groundwork for the growth of its digital economy. Hung Yen, about 50-60km southeast of Hanoi, has maintained steady momentum in implementing its digital transformation agenda, creating a stronger foundation for the province to advance science, technology, and innovation.

VIETNAM ECONOMY INVESTMENT

CHINESE INVESTMENT WAVE OPENS NEW DOORS

As Chinese companies move beyond factory relocation to ecosystem-driven investment, Vietnam has a rare opportunity to evolve from a low-cost production base into a strategic node in regional value chains. When global companies first diversified supply chains, the focus was largely on relocating manufacturing capacity.

VIETNAM ECONOMY INVESTMENT

VIỆT NAM STEPS UP EXPORT TO ACHIEVE US$550-BILLION TARGET

Việt Nam is intensifying efforts to sustain export momentum in the second half of 2026 as the country works towards its target of US$550 billion in export revenue for the year, despite continuing uncertainties in global trade. Statistics show that exports reached $266.5 billion in the first six months, meaning the economy needs to generate around $245.5 billion more during the remainder of the year to meet the annual goal.

VIETNAM ECONOMY INVESTMENT

ASIA POWERS VIETNAM’S SHRIMP BOOM, LEAVING THE WEST BEHIND

In the first half of 2026, Vietnam's shrimp exports surpassed the US$2.3 billion mark, driven largely by booming demand from China and a lobster craze. But behind that growth figure lies a lopsided picture: Asia is carrying the load, while the U.S. and Europe have yet to break out. These days, a container of frozen shrimp leaving a Ho Chi Minh City port is more likely to cross the East Vietnam Sea to Shanghai than the Pacific to Los Angeles.

Events Sponsors